Is the government punishing people with good credit?

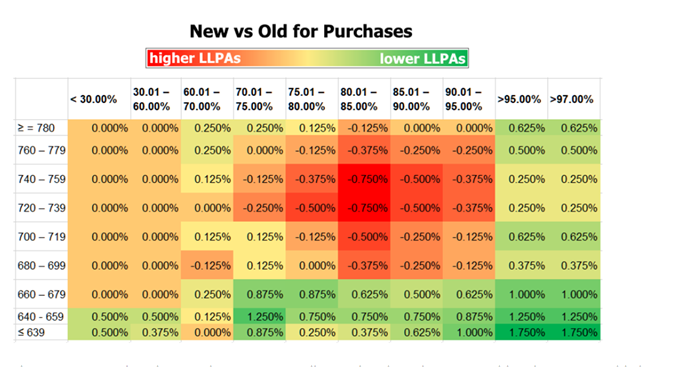

That is the headline that has been grabbing people’s attention this past week from various news outlets. So lets get down to brass tacks to use an old timey expression, are rates going up for people with good credit? The answer to that question is…mostly yes but with big caveats. The reason this change was implemented was because Fannie Mae & Freddie Mac, both are quasi government entities, wants to make a push to help first time home buyers and people with lower credit scores. Which is an admirable goal, but the piper always needs to be paid and in this case the people paying for this are the ones with good but not great scores. Specifically people with scores between 680-760 scores. Here is a heatmap which shows these new changes below (green means better pricing red means worse pricing). This applies to all loans through Fannie Mae & Freddie Mac which is the vast majority of loans in the US. This only applies to conventional and not government loans.

Verify your mortgage eligibility (Jul 18th, 2025)

There is too much to go over in one market update so here is breakdown of who benefits from these new changes:

People who benefit from these changes:

Verify your mortgage eligibility (Jul 18th, 2025)-First time homebuyers

-This is a huge boost to first time homebuyers, but only if they make less than 100% of the area median income (in Chester County that is $105,400). If someone fits that category then they are treated like someone with an 780 credit score. It doesn’t matter if they have a 640 credit score they will get better pricing then someone with a 780 credit score with putting 5% down. If they make more than 100% of the area median income then they do not get this benefit. Important reminder, anyone who hasn’t owned a home for three years is considered a first time home buyer

-People with credit scores over 780

Verify your mortgage eligibility (Jul 18th, 2025)-

The old threshold for interest rates was 740, the new threshold is 780 so people 780+ are pretty much avoiding any impacts from these changes

-People with income that is less than 80% of the area median income

-In Chester county this is $84,320. People in this category enjoy the same benefits as first time home buyers except there are even more benefits. On top of avoiding all of the rate impacts from their credit score they would also qualify for a $1,250 lender credit and possibly more depending on the loan amount. The good thing is we can pick and choose which income we can use to qualify them for. So if they make $80k in base salary and make $50k in overtime then we can just use base income, as long as they qualify for the mortgage with the base salary.

Verify your mortgage eligibility (Jul 18th, 2025)-People with under a 680 credit score.

-This group also sees improvement in pricing, there is a hit to having a score in this range just not as much as before

-People who put less than 5% down

Verify your mortgage eligibility (Jul 18th, 2025)-Pricing improved accross the board for anyone putting less than 5% down. First time homebuyers, regardless of income, can put 3% down instead of 5% down

People who do not benefit from these changes:

-People with credit scores from 680-760

Verify your mortgage eligibility (Jul 18th, 2025)-If you don’t meet the above criteria of being a first time homebuyer or in an income based program then pricing got worse pretty much across the board except if you put less than 5% in which case the pricing improved.

-People who want to put down 20%

-Even if your score is 780 there is a pricing hit to putting down 20%, unless your score is under 680 in which case there is a benefit

So there are some things I like but overall they could have done a much better job of structuring all of this. My biggest issue is that this is going to be hard to explain to borrowers. You can see with what I bolded that there are a lot of exceptions depending on what credit score that you have. It’s going to be confusing to a borrower with a score between 680-760 to say that you will be penalized for putting 20% instead of 5% down. All this to say is that there are going to be even more variables that go into determining interest rates so it’s an important reminder that the rate sheet that is being quoted is for top tier of credit.

Show me today's rates (Jul 18th, 2025)